|

1

|

- Stephen Chung

- Zeppelin Real Estate Analysis Limited

- HKIFM - China Real Estate Conference

- Shanghai, 7th

November 2008

|

|

2

|

|

|

3

|

- Devil’s Advocate?

- Challenging popular notions

- Testing the original arguments

- Debating for debating’s sake

- Hoping to obtain more vigilant arguments

- A Necessary evil?

|

|

4

|

- Courtesy of www.fluffyfeathers.com

|

|

5

|

- Black Swan?

- Biology: Cygnus Atratas

- JBook: The Black Swan by

Nassim Nicholas Taleb

- Black Swans: Events which cannot be predicted, both unpleasant and pleasant!

|

|

6

|

- Examples of Black Swans:

- Recent financial world crisis and the quick disappearances of big-name

investment banks, mortgage corporations…

- Asian Financial Crisis

- Great Depression 1930s

- Future Black Swans?

|

|

7

|

- Black Swans by definition are unpredictable events, and there is no way

to contemplate their existence, let alone to analyze them…

- But we can prepare ourselves for them, make allowances for their impact,

and strive through them…

- Main features of a Black Swan…

|

|

8

|

|

|

9

|

- & Huge impact!

- Losing shirt to realizing a dream

- Other features of Black Swans:

- Low in probability

- Stealth

- Make or break empires (now)

- Cause fundamental shifts (now)

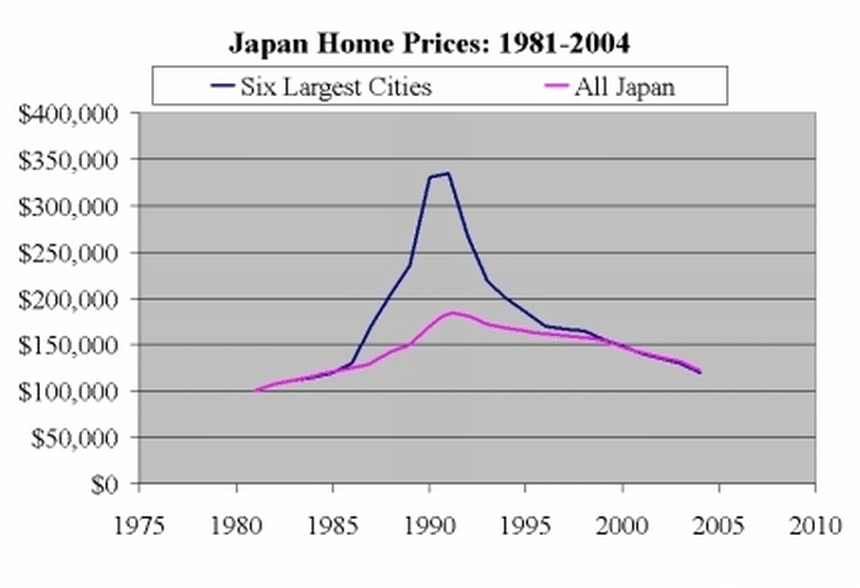

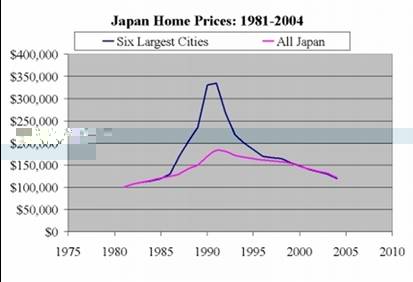

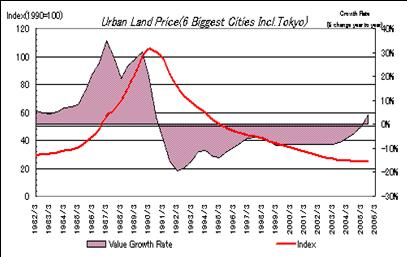

- Effects could last long (Japan)

|

|

10

|

- Over-confident people tend to get hit badly by unpleasant black swans:

- Via past successes

- Via grasp of knowledge and tools

- Via downplaying of randomness

- Via poor mind control of their own brains (built-in human tendencies)

|

|

11

|

- Because the brains have a tendency to find reasons for everything and certainty:

- Attributing one’s success to skills and effort (only)

- Worshipping economics and quantification tools e.g. Modern Portfolio

Theory

- Downplaying randomness (or luck if you like) because this means uncertainty

= threatening

|

|

12

|

- While we can’t seek out black swans, let’s see if we could find some gray

ones…

- Examine the reasons touted by both the optimists (Yea-Sayers) and

pessimists (Nay-Sayers)…

|

|

13

|

- China Real Estate Yea-Sayers:

- Urbanization Process

- Economic Growth

- Emerging middle class with aspirations and increased income

- Lack of good quality real estate stock to satisfy demand for quality

- Huge Savings and Reserves

- Let’s play

on the above…

|

|

14

|

|

|

15

|

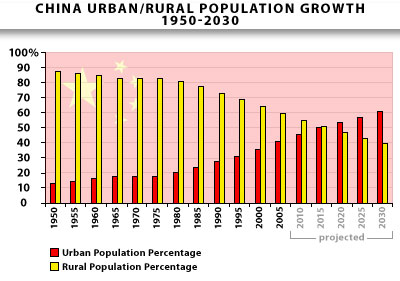

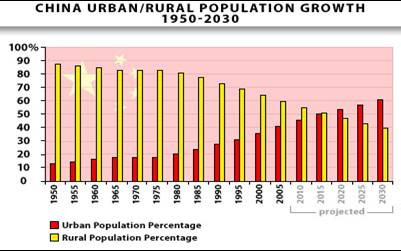

- Urbanization Process:

- Urbanization has been touted as a reason to expect growing demand for

private housing and rising house prices

- But this is putting the cart before the horse!

- Urbanization occurs because of economic activities and needs = a symptom

or result

- Urbanizing to urbanize = slums

|

|

16

|

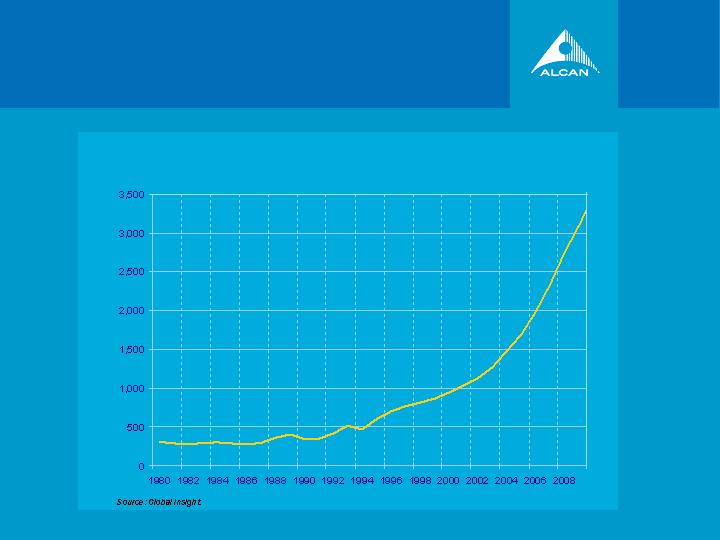

- Economic Growth: GDP per capita in US$

|

|

17

|

- Economic Growth:

- In GDP = But GDP does not account for wastage, breakage, or obsolescence

- Production in part still inefficient

- Straight-line projection but actual path could be non-linear

- Due also to the US$ Printing Press?

- Double-digit to single-digit

|

|

18

|

|

|

19

|

|

|

20

|

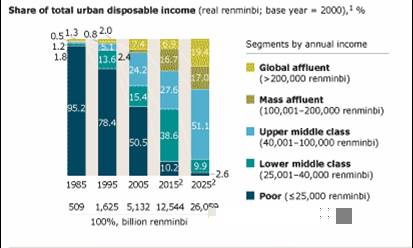

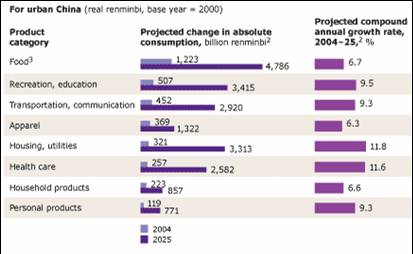

- Emerging Middle Class:

- Difficult to advocate the devil here

- Note 97% will be Middle Class or above in 2025…

- Note housing and health spending will be 10x current in 2025…

- Music to my ears!

- But wait! What about demographics?

|

|

21

|

|

|

22

|

- Emerging Middle Class:

- The housing splurge seen in developed economies (owing to baby-boomer

bulges) does not apply to China

- Relocation = rural to urban

- Upgrading = old to new / modern

- Watch out for asymmetry!

- Watch for cumulative-advantage!

|

|

23

|

|

|

24

|

|

|

25

|

|

|

26

|

- Lack of Good Quality RE:

- Good quality implies good design, good construction, and good management

- Quality, especially in the residential sector, has been improving

steadily over the years

- No doubt there are still bad developers, but there are also good ones

- But is good quality a deterrent to investment loss?

|

|

27

|

|

|

28

|

|

|

29

|

|

|

30

|

- Huge Savings and Reserves:

|

|

31

|

- Huge Savings and Reserves:

|

|

32

|

- Huge Savings and Reserves:

- Having huge savings and reserves may be comforting

- But they do not appear to always stop or prevent market downturns

- Hong Kong during the AFC 1997 to 2007: Correlations between home price

index, reserve, and M3

|

|

33

|

- Huge Savings and Reserves:

|

|

34

|

- To Yea-Sayers:

- Urbanization: Cause-Effect Mix Up

- Economic Growth: Cut the waste

- Emerging Middle Class: Beware of uneven distribution

- Lack of Good Quality RE: Having superb Micro RE features is no defense

against a Macro Down Trend

- Huge Savings and Reserves: ditto

|

|

35

|

|

|

36

|

- China Real Estate Nay-Sayers:

- Prices are (too) high

- Over-Supply

- Administrative intervention and market measures

- Immature markets and risks

- Lagging of legal-financial frameworks

- Let’s play

on the above…

|

|

37

|

|

|

38

|

|

|

39

|

- Prices Are (Too) High: Maybe

|

|

40

|

- Prices Are (Too) High: Volatile

|

|

41

|

- Prices Are (Too) High: Yes But

|

|

42

|

- Prices Are (Too) High: Yes But

|

|

43

|

- Prices Are (Too) High: Yes But

- Most global real estate markets are on the high side-cycle including

China’s

- Residential may be by 20% - 30% based on various parameters

- Many too-high opinions are based on average incomes

- Yet private housing = say top 50%

|

|

44

|

|

|

45

|

- Over-Supply: in construction

- Residential: as if 4,000,000 units @ 100 m2 GFA

- Office: as if 360 office towers @100,000 m2 GFA = ?

- Retail: as if 310 malls @200,000 m2 GFA = ?

- Residential: 4,000,000 / 400,000,000 households = 1%

- 4M / 200,000,000 = 2%

|

|

46

|

- Over-Supply: in construction

- But the important point is supply does NOT appear to correlate with

price much!

- For instance, Hong Kong prices peaked in 1997 yet supply was higher than

in latter lower price years

|

|

47

|

- Over-Supply: in construction

- Rather, it is the Supply to Demand Ratio which matters

- Supply is relatively inflexible = construction cannot stop at will and

high rises mean either hundreds of units in one go or none at all

- But demand can come and go quickly!

|

|

48

|

- Administrative Measures:

- All markets are administered, regulated, and / or guided

- In real estate = urban plans, building regulations, environmental rules,

realtor licensing, pre-sale guidelines etc

- Best to avoid interfering with price levels where possible

|

|

49

|

- Immature Markets:

- Generally, emerging markets like China may act and react less maturely

owing to fewer or no prior experience

- But then again recent events appear to suggest some people in developed

markets never learn

- Are emerging markets really more risky and volatile (all the time)?

|

|

50

|

- Lagging legal-financial infrastructures:

- Note it is “LAG” not “LACK”

- Improving gradually

- 1st tier cities > 2nd or 3rd tier

ones

- Wider breadth and deeper depth expected in years to come

- Typical real estate buying and selling is no big deal already

|

|

51

|

- To Nay-Sayers:

- Prices: up cycle, some over-$, but not worryingly high overall

- Supply: some but macro-wise not overly worrying

- Measures: appear to turn fiscal

- Immaturity: yes but mature markets are just as fickle-minded

- Infrastructures: a matter of time

|

|

52

|

|

|

53

|

|

|

54

|

- Yea Versus Nay: These too…

- Yea = going from US$2500/cap to US$5,000/cap is tough but not

impossible, “making it” category

- Yea = demographics => up the value chain, if achieved, means higher

income

- Yea = Credit crisis offers opportunities IF properly captured

|

|

55

|

- Yea Versus Nay: These too…

- Nay = Export customer economies slowing and Baby-boomers graying

- Nay = Credit crisis means less liquidity => affect asset prices

- Nay = Unintended [global] policy effects reducing free flow of capital

(investment), talent (knowledge), and trade (pricing)

|

|

56

|

- Gray Swans?: China RE

- No Decoupling = it will be affected

- Downtime likely = even Severe, Sharp, Short, and Sweet (to some)

- Contrary to some current opinions, some 1st tier cities will

offer great return, and NOT all 2nd or 3rd tier

cities will turn out to be as good as they are now being portrayed

- ASYMMETRY: 1-2 Global + 3-4 Regional + 8-12 Local ?

|

|

57

|

|

|

58

|

- From “Location, Location, and Location” which has never been quite

proven or right

- Via “Timing, Selecting, and Pricing”

- To “Liquidity, Liquidity, and Liquidity”

- IF Only 1 city is to be picked…

|

|

59

|

|

|

60

|

- Useful Resources and Acknowledgement:

- http://www.mckinsey.com/mgi/publications/china_Urban_Billion/slideshow/main.asp

- http://en.wikipedia.org/wiki/List_of_countries_by_GDP_(nominal)_per_capita

- http://www.real-estate-tech.com/articles/SRS080301.htm

- www.soufun.com

- www.yahoo.com

- www.dtz.com

- www.centaline.com

- www.cbre.com

- www.joneslanglasalle.com

|

|

61

|

- END

- Thank You

- www.Real–Estate-Tech.com

- Zeppelin Real Estate Group

|

備忘稿

備忘稿{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}